Financial aid is essential for many families, even more so now in light of COVID-19. How much do you know about this important piece of the college financing puzzle?

1. If my child attends a more expensive college, we’ll get more aid

Not necessarily. Colleges determine your expected family contribution, or EFC, based on the income and asset information you provide on the government’s financial aid form, the Free Application for Federal Student Aid (FAFSA), and, where applicable, the College Scholarship Service (CSS) Profile (a form generally used by private colleges). Your EFC stays the same no matter what college your child attends. The difference between the cost of a particular college and your EFC equals your child’s financial need, sometimes referred to as “demonstrated need.” The more expensive a college is, the greater your child’s financial need. But a greater financial need doesn’t automatically translate into a bigger financial aid package. Colleges aren’t required to meet 100% of your child’s financial need.

Tip: Due to their large endowments, many elite colleges offer to meet 100% of demonstrated need, and they may also replace federal student loan awards with college grants in their aid packages. But not all colleges are so generous. “Percentage of need met” is a data point you can easily research for any college. This year, though, some colleges that are facing lower revenues due to the pandemic may need to adjust their financial aid guidelines and set higher thresholds for their aid awards.

2. I lost my job after submitting aid forms, but there’s nothing I can do now

Not true. Generally, if your financial circumstances change significantly after you file the FAFSA (or the CSS Profile) and you can support this change with documentation, you can ask the financial aid counselor at your child’s school to revisit your aid package; the financial aid office has the authority to make adjustments if there have been material changes to your family’s income or assets.

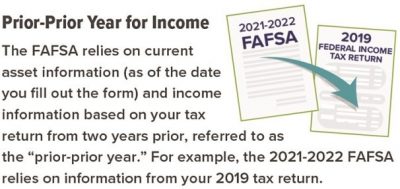

Amid the pandemic, annual income projections for some families may now look very different than they did two years ago based on “prior-prior year” income (see graphic). Families who have lost jobs or received cuts in income may qualify for more aid than the FAFSA first calculated.

Tip: Parents should first check the school’s financial aid website for instructions on how to proceed. An initial email is usually appropriate to create a record of correspondence, followed by documentation and likely additional communication. Keep in mind that financial aid offices are likely to be inundated with such requests this year, so inquire early and be proactive to help ensure that your request doesn’t get lost in the shuffle.

3. My child won’t qualify for aid because we make too much money

Not necessarily. While it’s true that parent income is the main factor in determining aid eligibility, it’s not the only factor. The number of children you’ll have in college at the same time is a significant factor; for example, having two children in college will cut your EFC in half. Your assets, overall family size, and age of the older parent also factor into the equation.

Tip: Even if you think your child won’t qualify for aid, there are still two reasons to consider submitting the FAFSA. First, all students, regardless of family income, who attend school at least half-time are eligible for unsubsidized federal Direct Loans, and the FAFSA is a prerequisite for these loans. (“Unsubsidized” means the student pays the interest that accrues during college, the grace period, and any loan deferment periods.) So if you want your child to have some “skin in the game” by taking on a small student loan, you’ll need to submit the FAFSA. Second, the FAFSA is always a prerequisite for college need-based aid and is sometimes a prerequisite for college merit-based aid, so it’s usually a good idea to submit this form to maximize your child’s eligibility for both.

4. We own our home, so my child won’t qualify for aid

It depends on the source of aid. The FAFSA does not take home equity into account when determining a family’s expected family contribution, so owning your home won’t affect your child’s eligibility for aid. The FAFSA also excludes the value of retirement accounts, cash-value life insurance, and annuities.

Tip: The CSS Profile does collect home equity and vacation home information, and some colleges may use it when distributing their own institutional need-based aid.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}